System

By positioning ethics as the priority value and building a infrastructure that includes organization, system and educational/promotional programs, we strive to become an ethical corporation while adapting to the internal and external environmental changes

Ethical Management System(3C)

-

-

Code of Conduct

-

Set Common Ethical Standards for Employees

-

- Code of Ethics

- Code of Ethics Implementation Guidelines

-

-

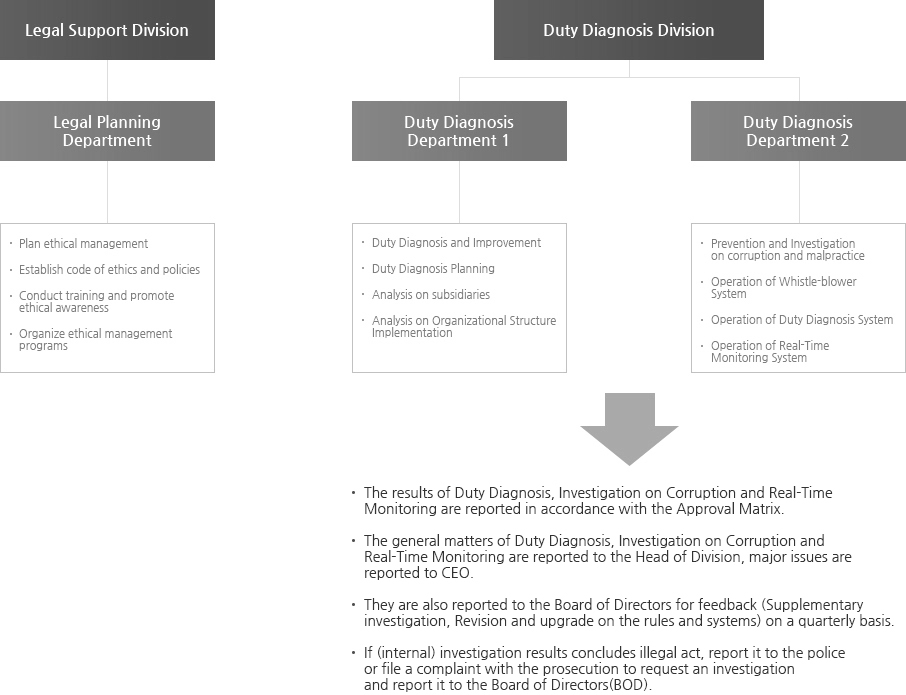

Compliance Check Organization

-

Establish an organization and a system to practice ethical management

-

- Audit Committee

- Legal Support Division

- Duty Diagnosis Division

- Ethics counseling office

- Whistleblower system

- Self-reporting system

- Ethics pledge

- Ethics & Compliance articles in partner contracts

-

-

Consensus by

Ethics education

-

Building consensus among employees and stakeholders on practicing ethical management

-

- Training & PR

- Ethics conference

- Campaign

- Integrated ethics management for all subsidiaries

- Ethics management support for subcontractors and suppliers

Ethical

Management

Ethical Management Organization

Management and Supervision on Ethical Management Activity

- Manages and supervises by Internal Accounting Control System

1. Internal Accounting Control System

- The system is designed and operated in order to secure trustworthiness of accounting information recorded and published according to the business accounting standard. It includes program for protection of the company asset and prevention of the unethical behaviors

- In order to prevent unethical behaviors, the control entries includes ethical management, reporting on violations, independence of the operating group, reporting to the board of directors and the audit committee which manage and supervise its operation, etc.

- (1) Code of Ethics, Code of Ethics Implementation Guidelines

- - Documentation

- - Definitions on classification and limits of unethical actions

- - Regular review on the updates

- - Easily accessible and legible publication for employees and officers

- - Index set-up identifying violations of Code of Ethics Implementation Guidelines

- - Annual scheduling and training for the Code of Ethics and compliance programs

- (2) Reporting on Violation

- - Enactment of rules and regulations and operation on reporting on the violations, protection and reward for whistleblower, etc.

- - Operation of Whistle-blower System(with anonymity or autonym)

- - Independent Investigation

- - For security, documented report to Board of Directors(BOD)

- - Report to BOD analysis and countermeasure on corruption actions

- (3) Evaluation on Ethics Implementation and Disciplinary Procedure on Unethical Behaviors

- - Ethical Management Performance result shall be included in HR assessment

- - Disciplinary procedure on personnel who violate the Ethical Standard is included in HR policy

- (4) Smart Auditor(Real-Time Monitoring System)

- - Real time Monitoring System is operated with massive unbiased data

- - The system refers to the previous unethical risks.

- - It monitors tendency and pattern on the cases by scenarios

- (5) Duty Diagnosis

- - Review on the possibilities of the various unethical risks when performing duty diagnosis

- - Annual planning and reporting on performance and results of duty diagnosis

- (6) Internal Audit Division and Manager

- - Designating the division monitoring steadily and evaluating the unethical risk. Defining the requirements for Internal Accounting Manager

- - Management of performance improvement

2. Internal Accounting Control System Procedure

3. Management and Supervision of Internal Accounting Control System

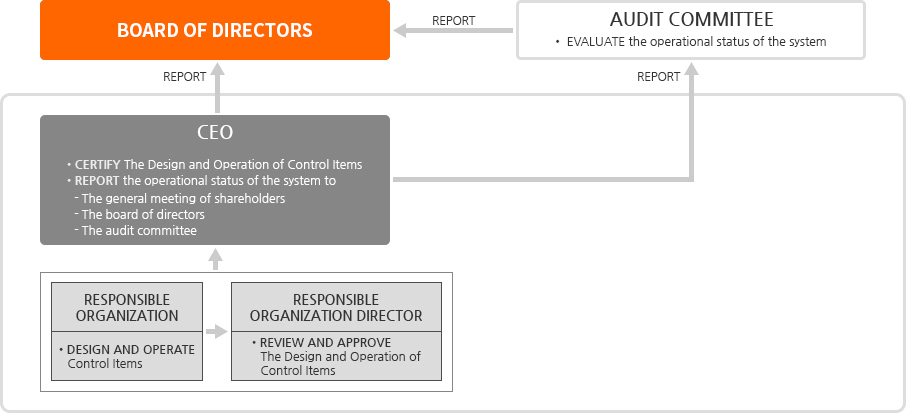

- CEO and Internal Accounting Manager : responsible for managing and supervising on the system

- BOD : responsible for the system which the company management designs and operates

- Audit Committee : responsible for evaluating on the system independently from the company management and supporting its appropriate operation and improvement.

4. Legal Basis

- Act on External Audit of Stock Companies, etc.

- The representative of a company shall report the operational status of the internal accounting control system of the relevant company to the general meeting of shareholders, the board of directors and the statutory auditor (if an audit committee has been established, referring to the audit committee) each business year:

- The statutory auditor of a company shall evaluate the operational status of the internal accounting control system; shall report the status to the board of directors in each business year; and shall keep such evaluation report at the head office of the relevant company for five years.

Corporate Auditing & Consulting Division

- Auditing & Consulting Department 1

-

Audit & Improve Business Process

- Audit planning

- General audit

- Special audit

- Fulfillment of audit result

- Auditing & Consulting Department 2

-

Investigate and prevent corrupt activities

- Planning of anti-corruption activities

- Tip-off investigation

- Special investigation

- Operation of Whistleblowing system

- Auditing & Consulting Department 3

-

Management diagnosis to subsidiaries

- Management diagnosis for subsidiaries

- Guidance for self-diagnosis

- Corruption investigation for subsidiaries

- Integrated ethics management with for all subsidiaries

- Audit commitee comprised of the board directors

- Corporate Auditing & Consulting Division supervised by the audit committee

- Regular reporting to the Audit Committee by Head of Corporate Auditing & Consulting Division who monitors corruption investigation and ethics compliance

CEO

- Management & Support Division

-

Compliance & Legal Support Department

- Ethic policy, standards, systems

- Ethics training· PR

- Fair trade regulations compliance

- Mutual growth policy with subcontractors and suppliers